How Are SMEs Protected Under The COVID-19 (Temporary Measures) Act? (Updated)

Lendingpot

July 21, 2022

(Updated)

The Singapore government has introduced additional measures to protect SMEs in the COVID-19 (Temporary Measures) (Amendment) Bill in Parliament on 5th June 2020.

On the 1st of April, the Ministry of Law (MinLaw) stated that they intend to introduce laws to offer temporary relief for those who are unable to fulfill their contractual obligations because of COVID-19.

These measures commenced on 20th April 2020 and will last 6 months (until 19th October 2020) in the first instance.

Measures Implemented (Including Amendment Bill)

SMEs will be protected via:

Temporary Relief from Legal Action

For contractual obligations that are to be performed on or after 1st February 2020 and;

Only for contracts that were entered into before 25th March 2020.

Measures will last 6 months, from 20th April 2020 to 19th October 2020. This may be extended to up to a year.

Measures relating to Bankruptcy and Insolvency

For individuals

Increase threshold for bankruptcy from $15,000 to $60,000

Extend statutory demand time limit from 21 days to 6 months

For businesses

Increase threshold for insolvency from $10,000 to $100,000

Extend statutory demand time limit from 21 days to 6 months

Rental Relief Framework for SMEs (Amendment) (for qualifying SME tenants of non government-owned / managed properties, Infographic)

Commercial Properties

Government provides 2 months rental waiver (Apr - May 2020)

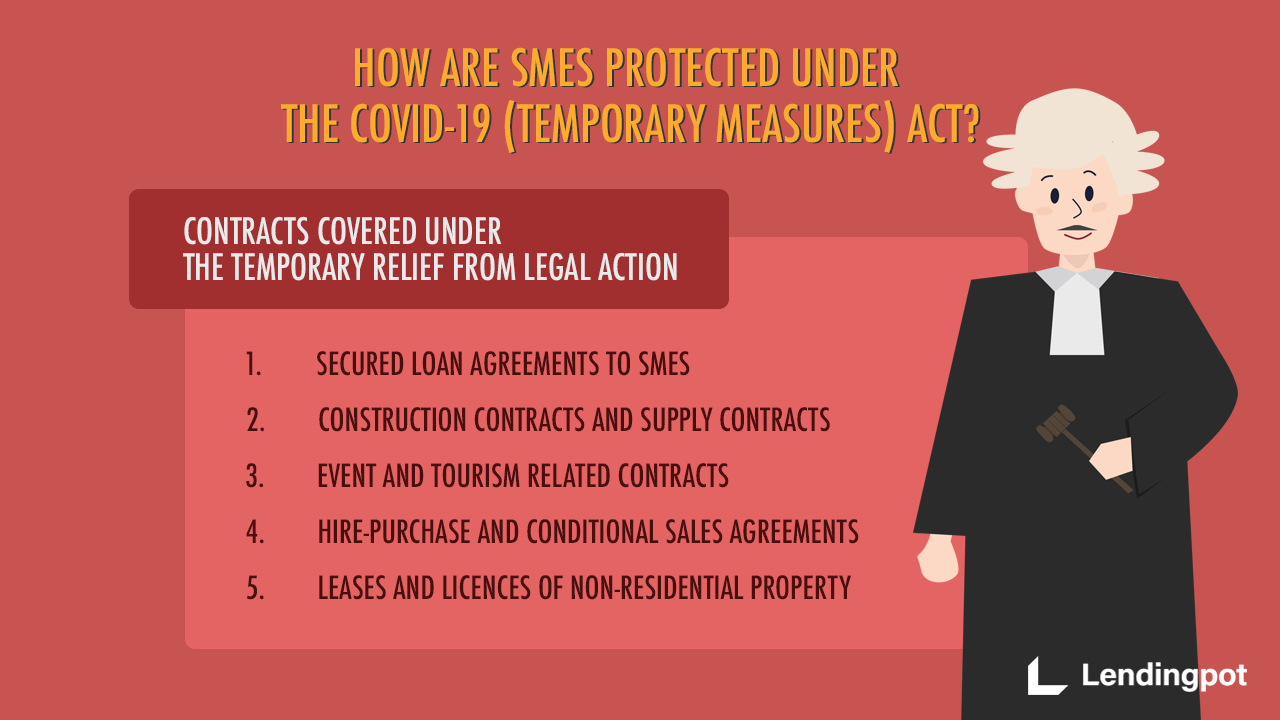

Contracts Covered Under the Temporary Relief from Legal Action

There are the 6 types of contracts covered by the act, as listed on MinLaw’s website.

Secured loan agreements to SMEs

Your creditor cannot enforce the security (i.e. over commercial or industrial property, plant or machinery used for business) located in Singapore

Your creditor cannot start or continue court or insolvency proceedings against you (during the prescribed period)

Construction contracts and supply contracts

The inability to supply goods or materials due to COVID-19 is a defence to a claim for breach of contract, damages or liquidated damages

The other part cannot call on any performance bond granted pursuant to the contract for the prescribed period

The other party cannot start or continue court or insolvency proceedings against you for the prescribed period

Event and tourism-related contracts

The vendor cannot automatically forfeit the client’s deposit

The deposit will be treated fairly, taking into account any expenses incurred by the vendor and alternative arrangements for the booking

The client cannot be made to pay cancellation fees (if provided in the contract) if the event / tour was to occur between 1st February 2020 to 19th October 2020 (dates inclusive)

Hire-purchase and conditional sales agreements

The financing company cannot repossess your plant, machinery or vehicle

The financing company cannot start or continue court or insolvency proceedings against you

Leases and licences of non-residential property

Your landlord cannot terminate your lease or evict you, on the basis that you have not paid rent

Your landlord cannot start or continue court of insolvency proceedings against you

Option to purchase & sale and purchase agreements with housing developers (Amendment Bill)

Booking fees or other consideration paid under Option To Purchase (OTP) cannot be forfeited

Sale & Purchase (S&P) and Agreement for Lease (AFL) cannot be terminated

The developer cannot impose new charges, increase charges or interest rates beyond what is provided for in the contract

Lendingpot.sg operates a Business Loan Marketplace that allows an SME to connect to multiple lenders with just one application, allowing the SME to know who its prospective lenders are and the rates that they offer, in a very short time.